Monsoon and food inflation

Context- The southwest monsoon had an abysmal start, arriving seven days late on June 8. Rainfall for the country was 52.6% below the normal (long period average) during the first two weeks, with 10.1% cumulative deficiency even at the end of June. The whole of eastern and southern India (except Tamil Nadu), besides Maharashtra, hardly got any rain.

Most of the major agricultural regions – save eastern Uttar Pradesh, Bihar, Jharkhand and West Bengal – have received normal rain.

(Credits- Indian Express)

Impact on sowing

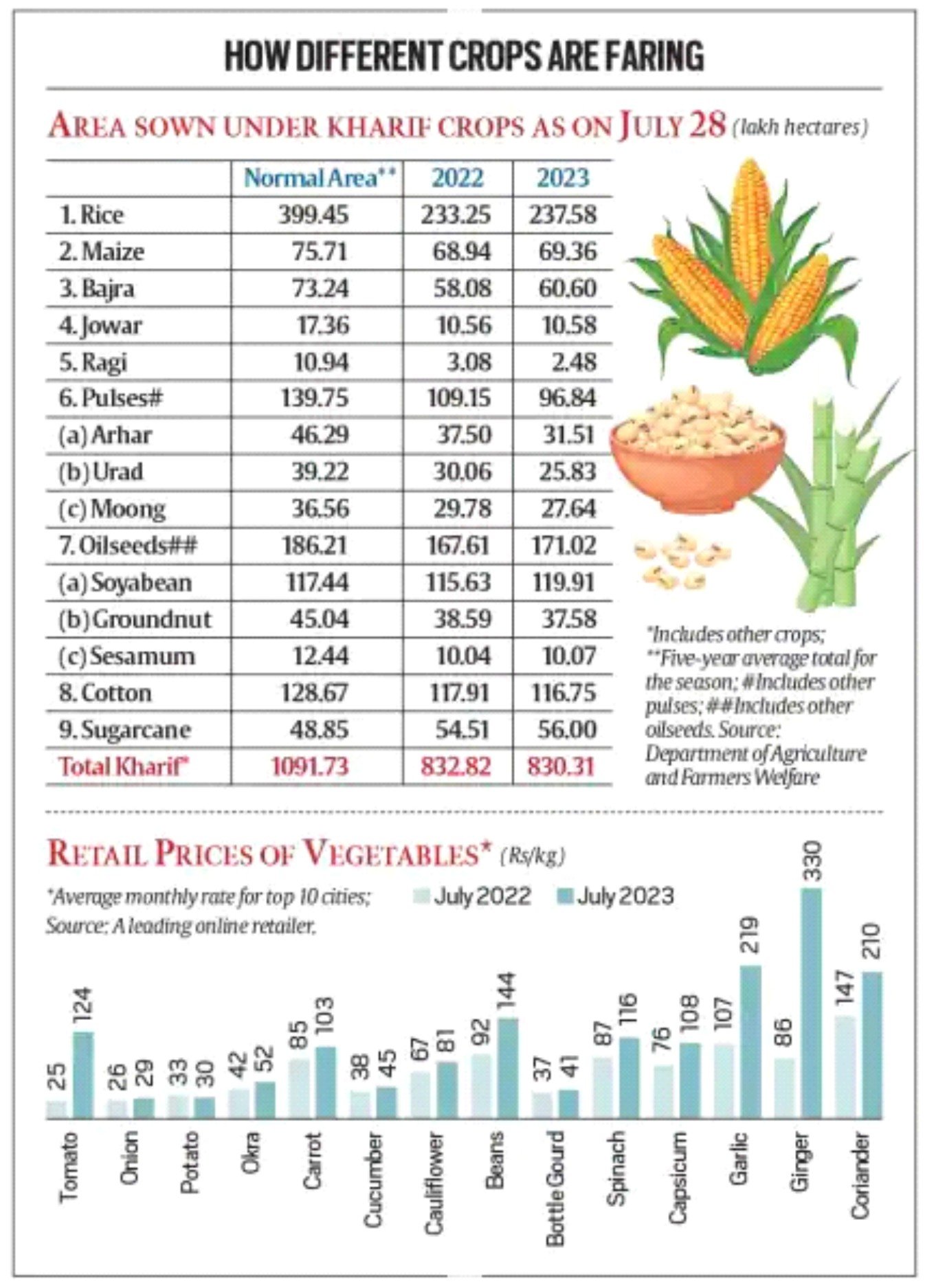

- The monsoon’s turnaround has led to a surge in kharif crop plantings – including the area under rice that was lagging behind last year’s levels till mid-July. But the gaps have since been significantly covered, barring in pulses, while forging ahead for rice (table).

- The bulk of kharif sowings happen from mid-June to mid-August. Rainfall in June-July decides how much area is covered. August-September rain matters for yields of the crops already sown. The same rain helps fill up reservoirs and ponds and recharge groundwater tables, which provide moisture for the subsequent rabi winter-spring crops.

- For now, the monsoon and kharif sowings have both been good. The initial worries, over whether there would be adequate rain to enable farmers to plant, are over.

El Niño caution

- In agriculture, well begun isn’t enough. In this case, the uncertainty relates to El Niño – an abnormal warming of the central and eastern Pacific Ocean waters off the coasts of Ecuador and Peru, known to suppress rainfall in India

- El Niño will gradually strengthen and peak during the winter months. All other things being the same, it would mean the monsoon entering a weak phase in August. If rainfall activity becomes progressively weaker, the impact can extend to the rabi season.

- That crop, dependent on stored rainwater, might take a bigger hit than the one already planted this kharif. Since winter rain is necessary also to sustain low temperatures, especially for wheat, it would be a double whammy.

The implications

- At 71.1 million tonnes (mt) as on July 1, rice and wheat stocks in government godowns were the lowest in five years for this date. That wouldn’t have mattered in a normal year, where there was some certainty about the coming crops and no major elections ahead.

- While rice acreage has picked up after mid-July, it’s not clear how much of that is under short-duration varieties of about 125-days seed-to-grain maturity.

- Had the rice belt, stretching from eastern to southern India through Chhattisgarh and Odisha, got rain on time, farmers may have planted more long-duration varieties of 150-155 days, yielding an extra 1-2 tonnes per hectare.

- There are reports of Punjab and Haryana farmers also having to undertake paddy re-transplanting in large areas along the Beas, Sutlej, Ghaggar and Yamuna rivers. This followed their already-planted crop suffering inundation from excess rain and water released from dams in Himachal Pradesh. Re-transplanting would, again, be of shorter duration varieties that usually yield less.

Other crops: Pulses and Edible Oil

- Among pulses, arhar (pigeon-pea) has registered the highest acreage dip. This is because of it being a 150-180 days crop grown mainly in Maharashtra, Karnataka and Telangana, which were rain-deficient during the sowing window that is generally till mid-July.

- Urad (black gram) area has also fallen, as farmers in Madhya Pradesh (MP), the largest producer, have chosen to plant more soyabean and maize.

- At the same time, the good rain in Rajasthan is expected to deliver a bumper crop of moong (green gram). Moong, like urad, is a 65-75 days crop and cultivated even in the rabi and spring/summer seasons.

- Edible oil inflation, too, is likely to remain low. This is primarily on account of imports, projected to top 15 mt, a new all-time-high, in the current oil year ending October 2023.

- Surplus monsoon rainfall in MP, Rajasthan and Gujarat should translate into excellent domestic harvests of soyabean, groundnut and sesamum this time, compensating for any import shortfalls from rising global prices.

Milk and vegetables

- The most encouraging picture is probably in milk, where February-March saw unprecedented shortages. Dairies in Maharashtra then paid up to Rs 38 per litre for cow milk containing 3.5% fat and 8.5% solids-not-fat. Ex-factory prices of cow butter and skimmed milk powder (SMP) hit Rs 430-435 and Rs 315-320 per kg respectively.

- From those highs, butter prices have now crashed to Rs 360-370 and SMP to Rs 260-270 levels, even as dairies are procuring milk at Rs 32-33 per litre. Supplies should further ease with buffalo calvings beginning from August.

Conclusion- High milk prices, plus improved fodder availability from both pre- and post-monsoon showers, are triggering the expected supply response from farmers at the right time. One can expect something similar in vegetables, where retail prices, not just of tomatoes, are high. It may show up in an unacceptably high consumer price index inflation number for July.

Syllabus- GS-3; Economy ; Environment

Source- Indian Express